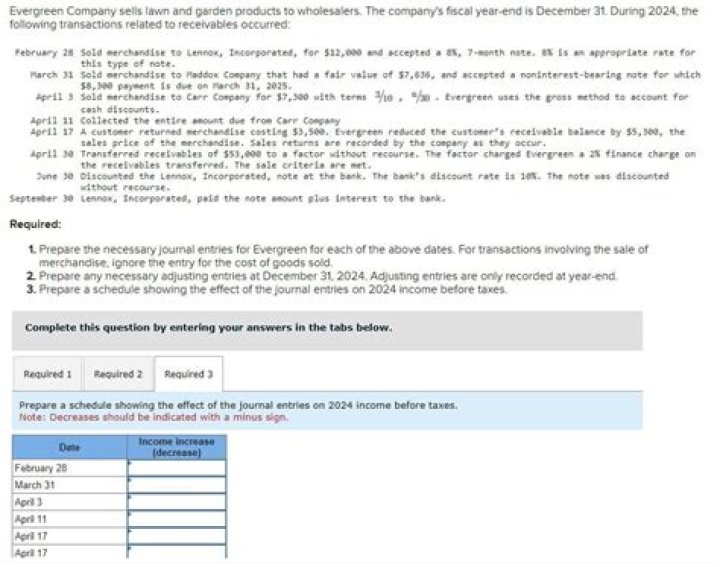

Evergreen Company Sells Lawn And Garden Products To Wholesalers

Evergreen Company Sells Lawn And Garden Products To Wholesalers

Help with accounting? 3

Evergreen sells gardening and horticultural equipment to dealers. The company's fiscal year ends on December 31. In 2011, transactions related to accounts receivable from users were as follows:

February 28 Lennox, Inc. Sell the product at $ 10,000 and receive a 7 month note payable at 10%. 10% off is a reasonable price for this type of ticket.

March 31, dox co. Sale of goods and recovery of interest free notes at 10% discount. As of March 31, 2012, 8,000 is due.

On April 3, the commercial goods were sold to Carr Company for 2 7,000 at 10/2, n / 30. Evergreen uses METD as a discount.

Carr Co. 11 sum of the total amount owed by

17 A customer returns an item for 3,200. Evergreen reduces the customer's outstanding balance for the sale of the item to $ 5,000. Sales returns are recorded by the company as they occur.

Assignment of اکا 50,000 to 30 accounts without any support to the receivable factor. This factor charges a 1% funding fee for claims made on Evergreen. Sales quality met.

June 30 Lennox, Inc. The invoice is sent to the bank. The bank discount rate is 12%. Tickets have been renewed without any support.

On August 31, Lennox, Inc. The bank pays interest in addition to a note.

Reason for liability:

1. Prepare the necessary journal entries for Evergreen for every five meetings. For transactions involving the sale of goods, ignore the cost of goods sold (keep all accounts to the nearest dollar).

2. Prepare the required adjustment entries before 31 December 2011. Adjustment entries are posted only at the end of the year (all accounts are in the closest dollar terms).

3. Develop a timeline to review the impact of manual accounting entries in 2011 income tax requirements 1 and 2.

1. Prepare the necessary journal entries for Evergreen for every five meetings. For transactions involving the sale of goods, ignore the cost of goods sold.

February 28

The doctor received 10,000 rupees.

10,000 crore sales

March 31

The doctor received Rs 8,000.

Discount crore ($ 8,000 x 10%) 800

7,200 crore sales

April 3

Doctor accounts receivable 7,000

Sales 7,000

April 11

Dr. Cash (98% x ,000 7,000) 6,860

Doctor Sales Discount (2% x ,000 7,000) 140

7,000 crore receivable accounts

April 17

Doctor sales are 5,000. Returns

5,000 crore accounts receivable

Dr. Stock 3,200

Production cost of goods sold 3,200

April 30

Dr. Cash (99% x $ 50,000) 49,500

Loss Doctor Accounts Receivable On Sale (1% x $ 50,000) 500

Receivable accounts of Cr 50,000

June 30

Dr. Interestable 333

Interest income crore ($ 10,000 x 10% x 4/12) 333

June 30

Dr. Cash (product below) 10,266

Loss of Doctor (Balance) in Sale of Receivable Documents 67

Receivable crore interest (from adjustment entry) 333

Exchange of accounts receivable from Rs.10,000 crore

Sum Assured $ 10,000

Flowers 583 *

10,583 on maturity

Discount (317) **

Cash receipts 10,266

* ($ 10,000 x 10% x 7/12)

** ($ 10,583 x 12% x 3/12)

August 31, 2011 - No registration required.

2. Prepare to publish the required provisions by December 31, 2011. Provisions are published only at the end of the year.

Doctor 600 discount

Interest income 600 crores ($ 8,000 x 10% x 9/12)

3. Develop a timeline to assess the impact of manual accounting entries in 2011 income tax requirements 1 and 2.

Date of increase (decrease)

February 28, $ 10,000

March 31, 7,200

April 3, 7,000

11 Apr (140)

April 17 (5,000)

April 17, 3200

30 Apr (500)

June 30, 333

30 June (67)

December 31, 600

Total impact $ 22,626

My profile is mesh with corn effect and Taurus moon ...