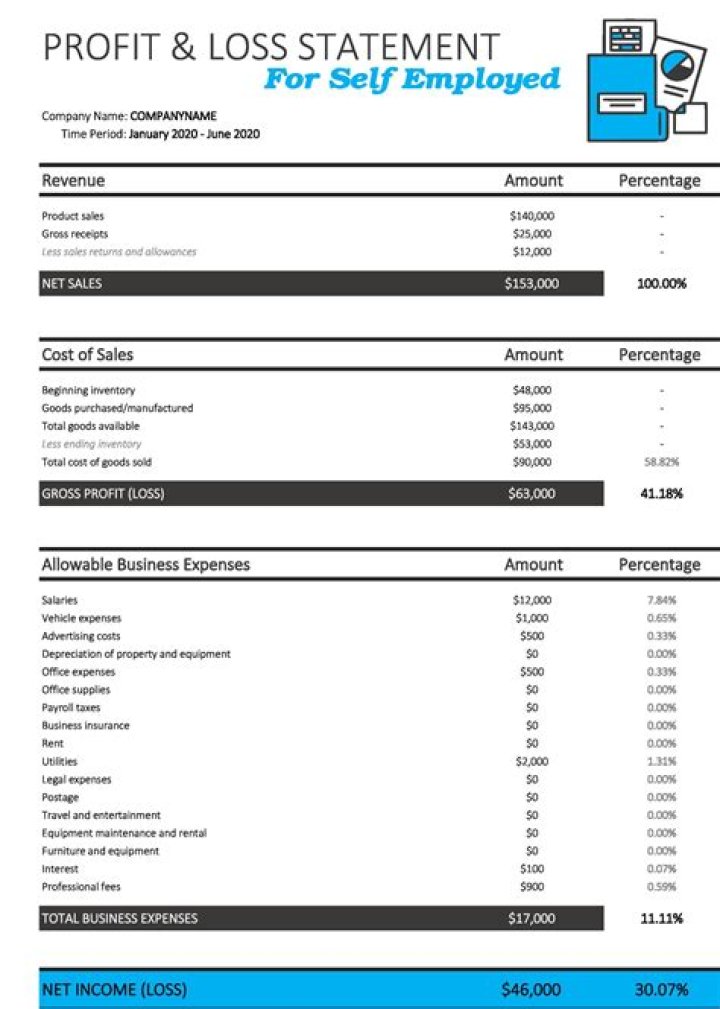

Profit and loss statement for self employed

How do I prepare a profit and loss statement? Preparing an income statement for a business involves calculating net income based on information such as revenue, net sales, cost of goods sold, gross profit, and operating expenses for a specified period of time as determined by the company. Edward Lowe Foundation.

How do you create a profit and loss statement?

You can create an income statement in a standard spreadsheet or with business finance software. 1. Create a table with three columns in the program of your choice. The first column is a description of the information it provides, the second is a list of findings, and the third is a list of additions.

What does a profit or loss statement tell you?

- Information about income or sales.

- Cost of sales or cost of goods sold (direct costs)

- Selling, general and administrative costs (overheads).

- marketing and advertising costs

- technological costs

- expenses as a percentage

- tax liability for the period

- Net profit company

How to prove loss of earnings for self-employed?

- financial condition. Even most small businesses maintain balance sheets and income statements as part of their general financial statements.

- Profit and loss account. The annual tax returns you file with the federal or state government are considered reliable proof of income.

- 1099s.

- Contracts.

How DOS a business use a profit and loss statement?

- annual comparisons. Look closely at the drastic changes, the drop in sales

- study trends. How is your company developing?

- Demonstrations Consider using the income statement to forecast future cash flows.

- Margin valuation, gross profit margin

- Sales: discover your most important months.

- Expenses.

- Income.

How do I calculate simple profit and loss?

- Select a time period. Do you measure the progress of your business monthly, quarterly or annually?

- List your business income for the period and break down the totals by month. List your income sources per month.

- Calculate your expenses.

- Determine your gross profit by subtracting your out-of-pocket expenses from your income.

- Find out if you're making money.

How do you calculate profit and loss?

Fast answer. To calculate profit and loss, estimate revenue, cost of goods sold, and costs incurred, then subtract cost of goods sold and cost of sales. A positive result means victory, a negative result means defeat.

How do you calculate profit or loss for a company?

How do you calculate profit or loss for a company?

- Add up all your monthly income

- summarize all your expenses for the month

- Calculate the difference by subtracting the total costs from the total income

- and the result is your victory or defeat

What is simple profit and loss?

What is simple profit and loss?

The income statement is a document that shows how a company's profit changes in the company's net income. This is achieved by subtracting all expenses from the revenue. Some income statements are very simple, while others are extremely complex.

What is a personal profit and loss statement?

What is a personal profit and loss statement?

Your income tax return lists your monthly income and expenses. The Personal Income Statement is similar to the Business Income Statement, except you keep track of your family's monthly income and expenses.

What is projected profit and loss statement?

The forecast income statement is part of the forecast financial statements prepared to show estimated future sales, expenses and net income and to calculate certain forecast ratios on your behalf.

How to create a profit and loss report in QuickBooks?

QuickBooks' income statement shows your income, expenses, and net profit or loss for the specified period. Follow the four steps below to create an income statement using the Report Center. This feature works the same between the 2011 and 2016 versions of QuickBooks. Select Reports > Report Center from the menu.

How do I run a profit and loss report on dates?

Select Reports > Report Center from the menu. On the Standard tab with Business and Finance selected, look for a report called Standard Income Statement. From the Dates drop-down list, select the date range for the report. Click the Run icon to view the report.

How do I view the profit&loss on the balance sheet?

How do I view the profit&loss on the balance sheet?

You can use the same method for the balance if you want to see it monthly. 1. Create a standard income statement (Reports > Business & Finance > Profit & Loss Standard).

How do you prepare a profit&loss statement?

How do you prepare a profit&loss statement?

How to prepare a profit and loss account? Many small businesses simply keep track of their income and expenses in a spreadsheet. They give it to their accountant at the end of the tax year and the accountant converts it into a professional income statement ready to file with HMRC.

How to create a P&L statement?

How to create a P&L statement?

- Find a format. If you're no longer using accounting software, spreadsheets like Excel or Google Sheets help streamline the process.

- Select a time period. Most companies calculate their profits and losses on a monthly, quarterly or annual basis.

- income list

- Calculate direct costs.

- Calculate the gross profit.

How to create a profit/loss statement?

How to create a profit/loss statement?

- Fill in the spreadsheet title with your company name and the time period shown in the income statement.

- Enter the total turnover and any discounts in the table. Calculate net sales.

- Enter your company's cost of sales in the table.

- Calculate your company's gross profit.

Why does your company need a profit and loss statement?

Why does your company need a profit and loss statement?

The income statement is important because it effectively reflects the amount of profit or loss a company has made over a period of time. That is why it is one of the most popular qualities. Every publicly traded company is required to publish its quarterly and annual income statement, its cash flow statement and its balance sheet.

What's an example of a P&L statement?

Example 1: XYZ ltd is active in the textile industry, producing and selling a variety of ready-to-wear. The company's policy is to prepare a monthly income statement and a full year income statement at the end of the financial year.

What are the main income statement ratios?

What are the main income statement ratios?

- gross profit. Gross profit is the money a company earns after deducting all raw material costs from sales.

- operating profit margin. Operating income is gross profit minus operating expenses.

- The amount of net profit.

- Sales, general and administrative management of gross profit.

- Depreciation and amortization to gross profit.

What is an income statement and what is it used for?

What is an income statement and what is it used for?

The income statement (also known as the income statement) uses your income and expenses to calculate your total net income (or loss) for the year. It is one of the most important accounting reports. This report is so important because it shows the overall profitability of a particular company.

What does a profit or loss statement tell you how to

Using the income statement you can: Answer the question, how much money do I make? Compare predicted performance with actual performance. To do this, compare your actual income statement with your budgeted income statement. Compare your performance against industry benchmarks. The ATO has many recommendations for the sector.

What is a profit and loss summary?

What is a profit and loss summary?

An income statement is a financial statement that summarizes a company's income and expenses for a period of time and is usually prepared annually or quarterly.

What is a profit statement?

What is a profit statement?

An income statement, also known as an income statement, is a financial document that shows managers, investors and other stakeholders the financial health of a company. The statement can cover a period of one day to ten years, but it is usually issued quarterly and annually.

What does a profit and loss statement tell you?

What does a profit and loss statement tell you?

The income statement basically tells the bank whether your business is profitable or not. While the bank balance tells you how financially stable you are. What you would normally want to see on the income statement is a steady increase in sales and net income.

What is a profit and loss statement and why is it important?

What is a profit and loss statement and why is it important?

Profit and loss statements are important because many companies are required to prepare them by law or by association membership. In addition, the income statement helps the company understand its net income, which can be helpful in the decision-making process.

What does a profit or loss statement tell you about real estate

What does a profit or loss statement tell you about real estate

The real estate income and loss statement simply displays the income and expenses of a property so you can see how much an investment is making or losing. Gross Income The first part of the income statement shows the gross income for the period.

What is a statement of profit and loss?

An income statement is a financial statement that summarizes income, expenses, and expenses incurred during a period of time, usually a financial quarter or year.

Is an income statement and profit and loss statement the same thing?

Profit and loss statements are sometimes referred to as profit and loss statements, but they are not the same as profit and loss statements. Both types of financial documents provide information about profitability, but their purpose, timing and users are different.

Profit or loss statement form

income statement form. The formula for a one-step income statement is as follows: Total Income Total Expenses = Net Income The income statement compares business income with expenses to determine a company's net income. Subtract the cost of sales from the sales proceeds to see the net profit or loss.

What is profit and loss template?

What is profit and loss template?

An income and loss model is used to create an income statement that summarizes the financial results of an organization over a period of time. Usually the period is a month, a quarter or a year. Also known as sample tax return.

What is a profit and loss sheet?

What is a profit and loss sheet?

The income statement is a continuous statement of a company's financial performance while the balance sheet is a snapshot of the company's financial position at the end of the year. In this sense, the income statement is an income statement and the balance sheet is a balance sheet.

What is profit and loss?

- Profit (P) The amount received from the sale of a product at a price greater than its cost.

- Loss (L) The amount the seller bears after selling goods at a price below cost is called loss.

- Cost Price (CP) The amount paid for the purchase of a product or item is known as the cost price.

What is profit and loss report?

An income statement, also known as an income statement, is a financial document prepared to show the profit or loss of an organization over a period of time. It contains an overview of the organization's total income and expenses. The difference between these two amounts is the amount of the gain or loss.

Free profit or loss statement

Free profit or loss statement

Free income statement templates are among the financial statements that a company is typically required to provide to shareholders. This is in fact an estimate of the income statement. The purpose of the report is to provide management with an accurate description of how the company has spent its resources over a period of time.

Can I get compensation for lost wages if I'm self employed?

It can be more difficult for freelancers to prove wage and income loss than for employees. If you cannot prove lost wages, you cannot receive compensation for it. That is why it is important to provide the insurance company or court with receipts and evidence. Thanks for subscribing!

How do I prove lost wages and income?

In order to prove lost wages and earnings, you will need to support your claim with documents and evidence: Proof of lost earnings and opportunities – This is how much you would have earned from the date of the accident until you have fully recovered.

How do I make a loss of earnings claim?

How do I make a loss of earnings claim?

To make a valid loss of income claim for your self-employed clients, they must collect documentation of the loss of income, income, and income as a result of the accident.

How to make proof of income for self employed?

The Form 1099 Self-Employed Tax Return and Payment shows your self-employed wages and taxes. It is considered one of the most reliable documents in existence due to its status as an official legal document. Your bank statements are another good answer to the question of how to verify your income.

How to prove loss of earnings for self-employed retirement

You must first prove your right to loss of income from employment using the least intrusive method, e.g. B. through self-generated receipts and reports. It is very easy to create an income statement in Quickbooks. Or you can create a table of your income and expenses to see trends and averages.

How do I Prove my income if I am self-employed?

Fortunately, whether you're self-employed or not, proving income is much easier than most people think. By having your tax return, tax return and bank statement in one place, you can easily verify your income.

How do I prove a personal injury claim if I am self-employed?

How do I prove a personal injury claim if I am self-employed?

If you are self-employed and claim compensation for lost income or lost income in a personal injury claim, you can substantiate this claim with the same type of financial documentation that you use to calculate income tax. Think of income statements, bank statements, previous tax returns, receipts, invoices, etc.

How do I prove loss of earnings with W-2 income?

Proving lost income with W2 earnings is easy: For example, if one of your clients at Sally Morin Personal Injury Lawyers is an employee of the firm, simply submit a form to your employer to see how much work your client lost when it was found.. accidents and what your salary is to calculate lost income.

What does loss of income insurance provide?

The purpose of the loss of wages insurance is to reimburse wages that you have lost as a result of an accident. This can be your hourly wage or an estimated amount that you will lose in disability due to injury. The exact terms and amount of the loss of cover insurance will be explained in your policy.

How to claim loss of business income with insurance?

Claiming loss of income from an insurance company Tell your insurer about your loss reduction plan. Notify your insurance company as soon as possible after you have suffered a loss. Application form. Lost business claims problems often stem from unrealistic or inaccurate payback times.

How do you calculate loss of earning capacity?

How do you calculate loss of earning capacity?

Calculation of incapacity for work. Typically, a future disability claim is calculated by taking the present value of the claimant's actual income, or estimated income, if underage or unemployed, up to age 65 (often the assumed conditional retirement date).

How do I prove income for my pandemic unemployment assistance claim?

How do I prove income for my pandemic unemployment assistance claim?

The EDD may ask you to provide proof of income to qualify for pandemic unemployment benefits. You have 21 days from the date of the email or written notice to prove your earnings in 2019 and avoid a reduction in your weekly benefit.

Does income from self-employment count as income for Social Security?

Some income does not count towards Social Security and should not be included in your net income calculation. For more information about becoming self-employed, paying Social Security taxes, and determining and reporting your net income, see If you're self-employed.

What is a Social Security earnings estimate?

Social Security asks for earnings estimates from people who have taken early retirement and have significant self-employment income or income that varies significantly from month to month. At the end of each year, Social Security sends these people a form asking them to calculate their income for the following year.

How to prove profit and losses?

How to prove profit and losses?

In addition, income statements generated by accounting software or even a simple Excel spreadsheet can help prove this loss. The problem with these auto-generated documents is that they can be modified for lawsuits. As a result, insurance companies and lawyers trust them less.

Why do you need proof of income when self-employed?

Proof of income is often required for credit, tax law and insurance. This can be intimidating for freelancers. In fact, proving your income is easier than you think.

What happens to your lost wages if you are self-employed?

What happens to your lost wages if you are self-employed?

They usually give a lot of discount on freelancers' lost wages until the cases are close to being processed. If you are an independent consultant or contractor, you will likely receive a Form 1099 from each of your clients at the end of the year.

What is self employed profit?

Take advantage of independence. The difference between an independent contractor's income level and expenses incurred when revenues exceed expenses and result in profit, as shown in the income statement.

What is self employment loss?

loss of independence. The difference between the amount of revenue earned by an independent contractor and the expenses incurred when expenses exceed revenues and result in a loss.

What is a profit and loss statement?

What is a profit and loss statement?

- Profit and loss (P&L) is an indicator of a company's health.

- The income statement is one of the most important documents you need to present to get money.

- This allows banks and investors to see the total income, debt and financial health of your company.

- With a little training and practice, anyone can create an income statement.

What is the formula for profit and loss?

Loss and profit can also be calculated as a percentage using the following formula: Loss % = (loss/cost) × 100. Profit % = (profit/cost) × 100. Example: John bought a bicycle for $339 and sold it to buyer for $382.

Do you need a profit and loss statement template?

Fortunately, this process can be made simple and straightforward with a self-employed income statement template. A profit and loss statement, also known as a profit and loss statement, is a tool that measures your company's profits (sales or sales) over a period of time.

Do I need a profit and loss statement If I'm self-employed?

From quarterly taxes to bills, freelancers deal with a lot of paperwork. While you are not required by law to file a profit and loss statement with the regulator, it is wise to prepare one so that you have a clear picture of what is happening with your company's finances.

What does net profit mean on a P&L statement?

Your net income (or loss) is the bottom line on your income statement. This is used to determine if a business is profitable and how much. If the result shows a profit, then you have earned more than you have spent. If the results show a loss, it means you spent more than you earned.

What does it mean when your profit and loss is negative?

If the number is negative, you have lost. Profit and loss reports help you determine what's going well in your business and what problems are holding you back the most. This information will help you create a business plan that will support your growth and set you on the path to success.

What is profit and loss income statement?

What is profit and loss income statement?

The income statement, also known as the income statement, is a financial statement that shows the net income (net income) and expenses of a company during a profit period.